Q2 2023 quarterly report: Results holding up in a challenging context

La Norteña’s agricultural engineer Francisco Esviza [right] with farmer Ramón Monges in the field of lemon verbena

Four times a year Oikocredit publishes key facts and figures on the previous quarter. Here we provide our investors and others with additional background context on developments during the second quarter of 2023.

Strategic plan 2022-2026: progressing community building and resilience

Oikocredit’s community-focused investment portfolio is growing, with new approvals for community-focused loans and increased collaboration with prospects for innovative partnerships. This is a key element in our 2022-2026 strategy involving a holistic approach to help low-income communities in our focus countries build resilience.

Oikocredit’s groundbreaking client self-perception survey is now in its third year and has 35 inclusive finance organisations participating (five more than we expected), with several involved for the third consecutive year. The survey provides insight into what is impacting the lives of our partner organisations’ end-clients and how we and our partners can support these people even better.

The cooperative’s community-focused strategy also embraces nurturing a global impact-making investor movement and facilitating more direct connections between partners, low-income communities, members and investors. We successfully completed the conversion of the investments in Germany to the new capital-raising model and made final preparations for the transition in Switzerland.

In Q2 we held the second event in our new online series, Oikocredit Live. Entitled Combatting Climate Change with Sustainable Solutions for Low-Income Communities, the webinar featured two partners: the Norandino agriculture cooperative in Peru and Kenya-based BURN, which manufactures and distributes fuel-efficient cookstoves. This continued our interactive conversation with members and investors about how the money they entrust to us helps make a difference in people’s lives. In parallel, we are developing Oikocredit Journeys for members and investors to visit partners and beneficiaries in a responsible manner. The first Oikocredit Journey is planned for 2024.

Organisational developments

Oikocredit’s annual general meeting (AGM) and members’ meeting in June involved further discussion about our transition to the new capital-raising model and creating an investor movement. Membership in the cooperative and the future of membership were also on the agenda.

We are working with the support associations on their role in stimulating engagement with current and potential investors and in offering activities related to global learning for transformation and advocacy. The latter aims to create awareness on topics close to our heart, for example on what constitutes responsible investing. Oikocredit’s global leadership group held its second meeting in Q2 to deliberate on the key objectives of the strategy and the actions needed to successfully implement the strategy in the coming years.

Portfolio developments and financial performance

Oikocredit has remained profitable, achieving a positive result in Q2 of € 3.8 million. Our annual social performance monitoring and regular assessment of partners’ environmental, social and governance (ESG) performance continue to highlight positive outcomes and increasing awareness of the importance of having a good ESG framework in place.

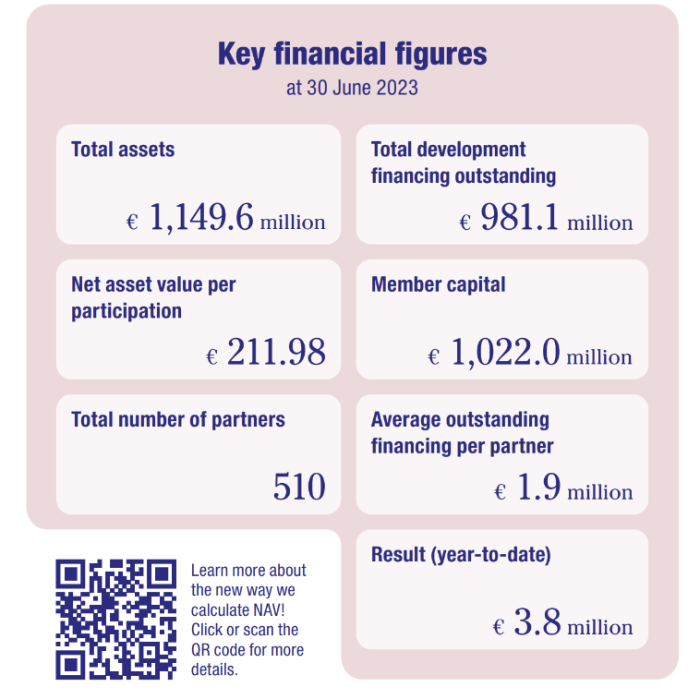

The development financing portfolio of credit and equity reduced by 2.9% from € 1,010.6 million to € 981.1 million. The decrease can be explained by external factors such as higher interest rates and the cost-of-living crisis, which supressed demand for credit among partners and increased risk for Oikocredit. Central to the new strategy, however, our portfolio of community-focused projects (education, community infrastructure, and so on) has grown to € 23.3 million. Total partner numbers have increased to 510 from 501 in Q1.

Portfolio quality came under pressure, with more partners delaying repayments because of limited in-country availability of dollars and the rising cost of hard currency compared to local currency. PAR 90 (the percentage of loans with repayments at least 90 days overdue) rose from 4.4% to 5.6% but remained below our 6% target threshold. Portfolio diversification helps us spread and mitigate risk, and we assess country exposure, investment type (credit or equity) and sector risk each quarter.

Loan write-offs, at € 7.0 million, were higher than in the first quarter, and increased loan loss provisioning for partners of € 4.7 million affected the net result. Operating income, margin and operational costs (the latter up from 3.2% to 3.5% of total assets) were in line with expectations. To maintain effective cost controls, we hold quarterly cost-monitoring meetings across the organisation. Liquidity decreased as projected, from 22.5% to 19.9%, although this is still fully sufficient to fund redemptions and new lending and equity investments.

Investor capital reduced to € 1,022.0 million from € 1,097.6 million. This was expected with the transition to the new capital-raising model, as we anticipated some members and investors would decide to redeem their capital. By the end of Q2, all outstanding shares were converted to our new investment product, participations. As of 1 July, Oikocredit directly offers participations in Austria, France, Germany, Italy (Südtirol), Spain, Sweden and Switzerland, while the Belgian and the Dutch markets are still served by Oikocredit Belgium and Oikocredit Nederlands Fonds respectively. More than 80% of all member capital has transitioned to our new capital-raising model. As always, we value our members’ and investors’ commitment to Oikocredit’s mission.

Net asset value (NAV) under our revised calculation method decreased from € 212.36 per share to € 211.98 per participation partly due to the dividend distribution in June of €5.6 million decreasing the member capital. The main driver for the decline originated from the larger decrease of the total distributable assets compared to the market value of the member capital.

Outlook

The 2022-2026 strategic plan, which aims to create resilience in many ways, has shown its first fruits, and we have promising new community-focused and resilience-building projects in the pipeline for roll-out later this year. We will publish our latest Impact Report in the coming months, showing our work reaching more end-clients with fair and responsible practices. The cooperative has started preparations to report for the first time in 2026 under the EU Corporate Sustainability Reporting Directive.

We are cautiously optimistic about the second half of 2023, despite the economic challenges across Africa, Asia and Latin America and impact of the war in Ukraine. Alongside social impact, we expect to continue to generate a positive financial result.

To help improve our digital services for partners and investors, we will implement several IT and change projects in the coming period, including enhancements to our online partner and investor portal and the introduction of a complaints mechanism.

Working with the support associations, we will expand awareness-raising and capital-raising activities. Within the cooperative, deliberations on membership will continue.

More information about Q2 2023 is available at https://www.oikocredit.coop/en/about-us/facts-figures/facts-figures.

| Title | Filesize | MIME-type | ||

|---|---|---|---|---|

| Oikocredit in Q2-2023 (PDF) | 3.2 MB | application/pdf |

Archive > 2023 > August

- 24/08/2023 24/08/2023, 11:53 - Supporting Peruvian MSEs through digital lending

- 24/08/2023 24/08/2023, 11:45 - Peruvian Fintech Prestamype closes a US$5 million Pre-Series A equity round led by impact funds ALIVE Ventures and Oikocredit

- 23/08/2023 23/08/2023, 14:04 - Q2 2023 quarterly report: Results holding up in a challenging context

- 17/08/2023 17/08/2023, 11:18 - Financial inclusion – what is a fair interest rate?

- 01/08/2023 01/08/2023, 13:16 - Oikocredit, IDB Invest and Cooperativa Jardín Azuayo announce groundbreaking diversity and inclusion social bond

- 01/08/2023 01/08/2023, 12:51 - Oikocredit, IDB Invest and Cooperativa Jardín Azuayo announce groundbreaking diversity and inclusion social bond